June was a brutal month for global equities, capping the worst first half of a year since the launch of the MSCI All Country World Index in 1987. For indices with longer track records, the story is worse. In the case of the US S&P500, the first-half performance has not been this bad since 1962. Global bonds were also deeply negative, leaving global dollar-based investors with almost nowhere to hide.

As a rugby or football commentator might say, it was a first half to forget. Next, they will ask if the performance can improve in the second half. History shows it is possible, as indicated by chart 1. However, given the depth of the decline and the murky macro backdrop, it seems unlikely that the first-half losses will be reversed in the second half. Recovery could take time but will happen eventually.

Equity markets move up and down over the short term, but the longer-term trend is upwards.

Chart 1: MSCI All Country World Index returns, in dollars

Source: Refinitiv Datastream

The reasons for the declines across asset classes are well-known by now but can be summarised as follows.

Expectations of inflation and interest rates have been marked up substantially since January, while expectations for global economic growth have been notably reduced in recent weeks. The ongoing Russian invasion of Ukraine takes much of the blame, but inflation was already rising rapidly late last year, partly because of strong consumer demand, and partly because of Covid-induced supply disruptions.

Inflationary pressures

There are some signs that inflationary pressures are easing. Commodity prices are off their recent peaks, supply chains are unclogging, and consumer demand seems to be shifting from durables to services. China is declaring victory over Covid (for now), meaning that its massive productive capacity can return to running full steam.

At the same time, inflationary pressures from services like housing, health and leisure are rising. These are much more local in nature and also more closely linked to trends in the labour market. Service inflation also tends to be stickier. If it is low, it tends to stay low. But if it is high, it also tends to stay high.

The net result is that while overall inflation could start declining in the months ahead in developed countries, it will likely remain elevated as the second half of the year draws to a close.

Certainly 2% targets in the US, UK and Europe are far away (Japan is another matter).

This has two consequences: firstly, if the cost of living increases faster than wages and salaries, consumers face falling real incomes that force them to eat into savings or borrow to maintain consumption. Thus far, in the US, they’ve been able to rely on savings buffers. However, while ample, those savings are not infinite. In poorer countries, those buffers are close to non-existent.

Secondly, the more elevated inflation remains, and unless there is a strong indication of a downward trend, central banks will feel compelled to maintain interest rate pressure. As Federal Reserve Chair Jerome Powell noted last week at the annual central banking conference in Sintra, Portugal, bringing inflation down is “highly likely to involve some pain, but the worst pain would be from failing to address this high inflation and allowing it to persist.”

Sceptics might note that the pain – unemployment – will not be felt by central bank chiefs who have statutory job security. Moreover, as any first-year economics student will tell you, monetary policy works with a lag of one to two years. By the time the evidence of declining inflation is clear, it might be too late to turn course, and higher interest rates could already have caused significant damage to the economy and company profits.

There are other risks too.

The war in Ukraine shows no sign of resolution and an escalation is possible with unpredictable results. This includes shutting off energy supplies to Europe. Meanwhile, as the European Central Bank tightens policy, a repeat of the 2011-12 fiscal crisis will be on their minds. It was 10 years ago in July 2012 that Mario Draghi, then ECB President, promised to do “whatever it takes” to prevent the Eurozone from breaking apart. His successor, Christine Lagarde, is striking a similarly forceful tone, but it is focused on fighting inflation. She might be forced to abandon it.

Asset class performance

Getting into the specifics of asset class returns, most of the pain this year has been felt by growth shares that are more sensitive to higher interest rates and were more expensive to begin with.

However, value shares are typically more sensitive to the economic outlook and were also deeply negative in June. The MSCI All Country World Growth Index lost 8.5% in June and 27% in the first half of the year. The Value Index similarly lost 8.7% in the month, but its year-to-date decline is less severe at -12.5%.

From a country point of view, the US market remains the most important as it makes up around 60% of global benchmarks. The S&P500 lost 8.3% in June and 19.9% since the start of 2022. Other indices fared even worse. The Russell 2000 Index of smaller companies has lost 24% this year while the tech and growth-heavy Nasdaq lost 30%.

Emerging markets were also negative in June, but a turnaround in Chinese shares as the country’s Covid lockdowns eased limited the damage. For the six months to end June, the MSCI Emerging Markets Index is down -17.5%, the third worst first half since the launch of the index, behind only 2008 and 1998.

In international bond markets, returns for the first half are among the worst on record. Not only did bond yields shoot up, but they also did so from extremely low levels. Investors suffered price declines with limited offset from interest income.

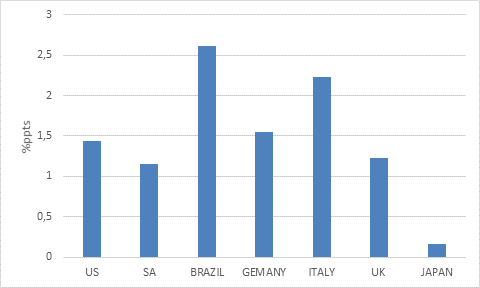

The benchmark US 10-year Treasury yield was only slightly higher during the month at 2.9% but hit a decade-high of 3.5% intra-month. Since the start of the year, it has doubled. The equivalent German 10-year bond yield shot up from -0.1% to 1.3% during the first six months. Moves at the shorter end of the curve were even more dramatic as they more closely reflect central bank policy rates. The yield on the 2-year US Treasury note rose from 0.7% to 2.9% since the start of the year.

For investors in corporate bonds (and riskier sovereigns such as Italy) there was a double whammy as spreads over the safest bonds widened.

Chart 2: Increase in 10-year government bond yields in 2022

Source: Refinitiv Datastream

Finally, the performance of the dollar in the first half of 2022 is also notable.

While the Russian invasion and subsequent sanctions led to renewed predictions of the dollar’s demise, it responded by surging to a 20-year high, supported by a continued widening of interest rate differentials. It gained 8% against the euro, 9% against the pound and an incredible 17% against the yen since the start of the year. These are big moves for developed market currencies.

Home ground advantage

June was a rough month for local asset classes too.

However, it should be noted that South African investors are better off over the past year than their peers in America and Europe.

South African assets were cheaper at the start of the year. Cheap investments don’t escape market sell-offs, but they often fall less since there is less hot air that needs to come out. The exchange rate has also softened some of the blows of declining global markets.

In terms of local equities, the FTSE/JSE Capped SWIX lost 7.5% in June, pulling year-to-date returns into negative territory at -4.6%. The one-year return of 6.9% is still ahead of cash and inflation, but only marginally.

Chart 3: Asset class performance in 2022 in rands

Source: Refinitiv Datastream

Listed property was also deeply negative in the month. The FTSE/JSE All Property Index (ALPI) lost 10% in June, pushing year-to-date returns further into the red. The 12-month return is now also slightly negative.

South African long bond yields have risen by a similar amount as US yields (chart 2 above) since the start of the year and therefore the All-Bond Index has delivered a negative return of -2% this year. However, the increase comes on top of already elevated yields. Therefore, the total return of local bonds has been much better than global bonds as interest income could offset some of the price declines.

Finally, sentiment turned against the rand over the past few days as the implications of Stage 6 loadshedding weighed, but for the most part the currency has responded to global forces. It has been supported by elevated commodity prices, while a stronger dollar has exerted downward pressure. The rand is only slightly weaker against the dollar since January, but it is down 14% compared to a year ago, providing local investors with some respite from the declines in dollar asset values over that period. The rand only depreciated around 1% against the pound and the euro over the past 12 months.

All in all, while volatile, the rand has been remarkably resilient given the global market turmoil.

Rolling with the punches

The returns scoreboard is not looking pretty. It is clearly a challenging environment for investors, and no-one likes to experience steep declines in asset values, especially retirees who have less time to recover from setbacks like these.

Here it is important to let go of the sporting analogies. A coach can give a stirring half time pep-talk and the players can charge back onto the field and play with more fire and determination. Investing doesn’t work like that.

Today’s returns are the result of investing decisions made well in the past. The decisions made today will determine returns well into the future.

This has two dimensions. The first relates to valuation. Market sell-offs present opportunities to buy asset classes and individual securities at more attractive levels. Current valuations are now below longer-term averages for the main asset classes, and this bodes well for longer-term returns. Unfortunately, this doesn’t tell us anything about what the market will do in the next few months, which is what most people would want to know right now. The reality is no-one knows.

Secondly, investors’ reactions to market corrections are crucial. Unlike sportsmen and women who control their bodies, and try to control the ball, individual investors do not control markets. They just have control of how they react to market events. The scarier the headlines, the greater the temptation to abandon their investment strategy. The boxer Mike Tyson put it more colourfully when he said that “everyone has a plan until they get punched in the mouth”. Remember that by the time you read about something in the news, it has already been discounted by markets. Responding to headlines is as the legendary rugby commentator Bill McLaren once dismissed the efforts of a Scottish lock, “as much help as a lighthouse in the desert.” The market punches were flying in the first half, but we need to stick to the plan.

The plan is to be appropriately diversified and focus on valuations, not volatility.

Old Mutual Wealth investment strategist Izak Odendaal.

Stay connected with us on social media platform for instant update click here to join our Twitter, & Facebook

We are now on Telegram. Click here to join our channel (@TechiUpdate) and stay updated with the latest Technology headlines.

For all the latest Business News Click Here

For the latest news and updates, follow us on Google News.

Denial of responsibility! NewsAzi is an automatic aggregator around the global media. All the content are available free on Internet. We have just arranged it in one platform for educational purpose only. In each content, the hyperlink to the primary source is specified. All trademarks belong to their rightful owners, all materials to their authors. If you are the owner of the content and do not want us to publish your materials on our website, please contact us by email – [email protected]. The content will be deleted within 24 hours.